73% Drop in Long Option Theta Decay, Buy Options Smarter | Outlier Insights

Announcements.

I’m looking for YOUR FEEDBACK. Week 2 with Substack for the newsletter and I think we’re figuring it out. I’m self taught on all this media stuff and it’s a completely new skillset so we’re doing it live! If you have a a few minutes, please fill out the GForm to let me know how I’m doing and what I need to work on!

Link to the next Monday Night YouTube Live at 5pm PT. Come with your questions, recent trades or trade ideas. Stay for the shotty humor. We’ll have the second live session at 5pm PT on Thursday!

Resources.

💡 Join the FREE Outlier Community Discord

📺 Join the weekly Monday Night YouTube live session

📈 Join on Patreon for weekly workshops, exclusive content & support the channel

🦅 Follow on Twitter for Investing Updates

Outlier Insights.

Week Ahead - 17July

Earnings have kicked off, with DAL, PGR, C, WFC, and JPM completed and there are some interesting initial trends I’m seeing. First, airlines look healthy with positive outlook from DAL that led to sympathetic moves in the other airlines, which begin reporting later next week. We saw a better than expected EPS but a negative forecast in C (1.31 est v 1.33 actual EPS), which moved 5.9% intraday (opened $48.48 and closed $45.75). You might’ve thought this would carry over to JPM and WFC and you would’ve generally been correct. JPM had a significant beat ($3.62 est vs. $4.75 actual EPS), but still closed lower on the day on guidance - this highlights in a very real way the weight of future expected performance. We’re seeing overall resilience in the banking sector but the slowing economy is prevalent. If you have some time to review

Buying Options Smarter

This post is for new options traders that like to buy options. The goal is to share some details that may help us reconfigure how we think about buying options.

There’s a bad habit of buying the cheapest option available and more often than not that includes a <60 DTE, far OTM option. While this may seem cheapest up front, this is actually a pretty costly behavior, for 3 big reasons:

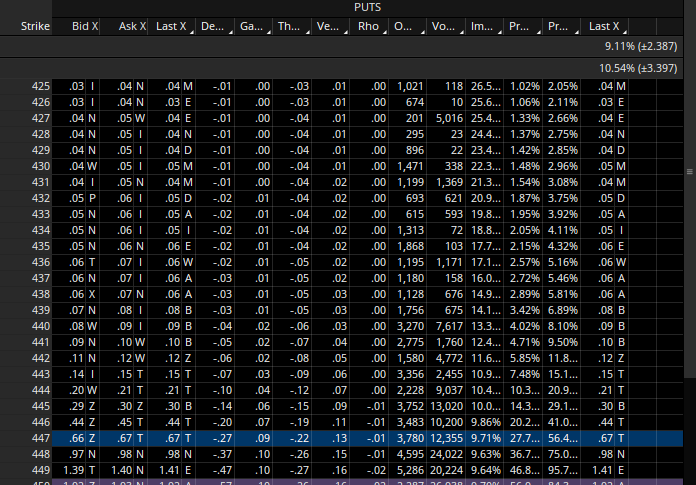

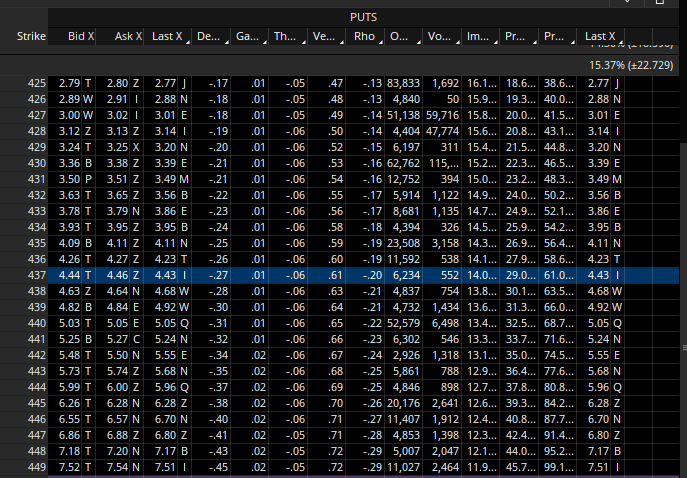

The closer DTE we buy, the higher theta decay is (take a look at 1a and 1b below, where adding just 61 days decreases theta decay by 73%). Within 60 DTE the rate steepens meaningfully and becomes exponentially worse. Fix: test out buying longer DTE options, I like at least 90, more often closer to 180. These cost more up front, but decay more slowly. I tend to buy 180+ and manage as I get within 90 DTE, so I tend to recoup most of the outlay.

1a. 3DTE SPY 0.27 delta put with -0.22 theta

1b. 62DTE SPY 0.27 delta put with -0.06 theta Far OTM options benefit from decreased overall theta decay (because there’s less extrinsic value in them, so less to decay. Remember, highest theta is ATM) which is nice but require larger moves to make money. This is due to the low deltas and low gamma. These options CAN compound into large returns (this is typically where you’ll see those several hundred % returns) but they need a big move, that we don’t always get. Fix: try buying options that have a higher delta (while more expensive, there’s still good leverage) I prefer 0.80+. If we want to add those cheap kicker options, in case we get a big move that’s cool, but by having the base position being deep ITM we have a better opportunity to make money on average.

Mindset for these short DTE far OTM plays typically involves the word “lottos” where we absolve ourselves of culpability if it doesn’t work and expect to lose our full investment. This is similar to simply buying lottery tickets - and tends to have a similar expected return.

The simple adjustment of combining longer duration with deeper ITM long options, we reshape the behavior of the position and get close to one of my go to strategies - Ratio Diagonals (can use calls to play bullish thesis and puts to play bearish). Happy to dive more into those if people are interested. If you find these posts helpful, don’t forget to share and subscribe!